India runs on more than one kind of currency, and one of them is faith. Every credible estimate agrees temples move a genuinely large amount of money through the Indian economy. Almost nothing else about the number is agreed upon. Depending on which source you read, India's "temple economy" is worth $40 billion, or $58 billion, or over $200 billion, and each of those figures is measuring something slightly different. That confusion is itself the story, because it tells you how little standardised accounting exists for one of the oldest economic institutions in the country.

Chapter 1How big is India's temple economy, really?

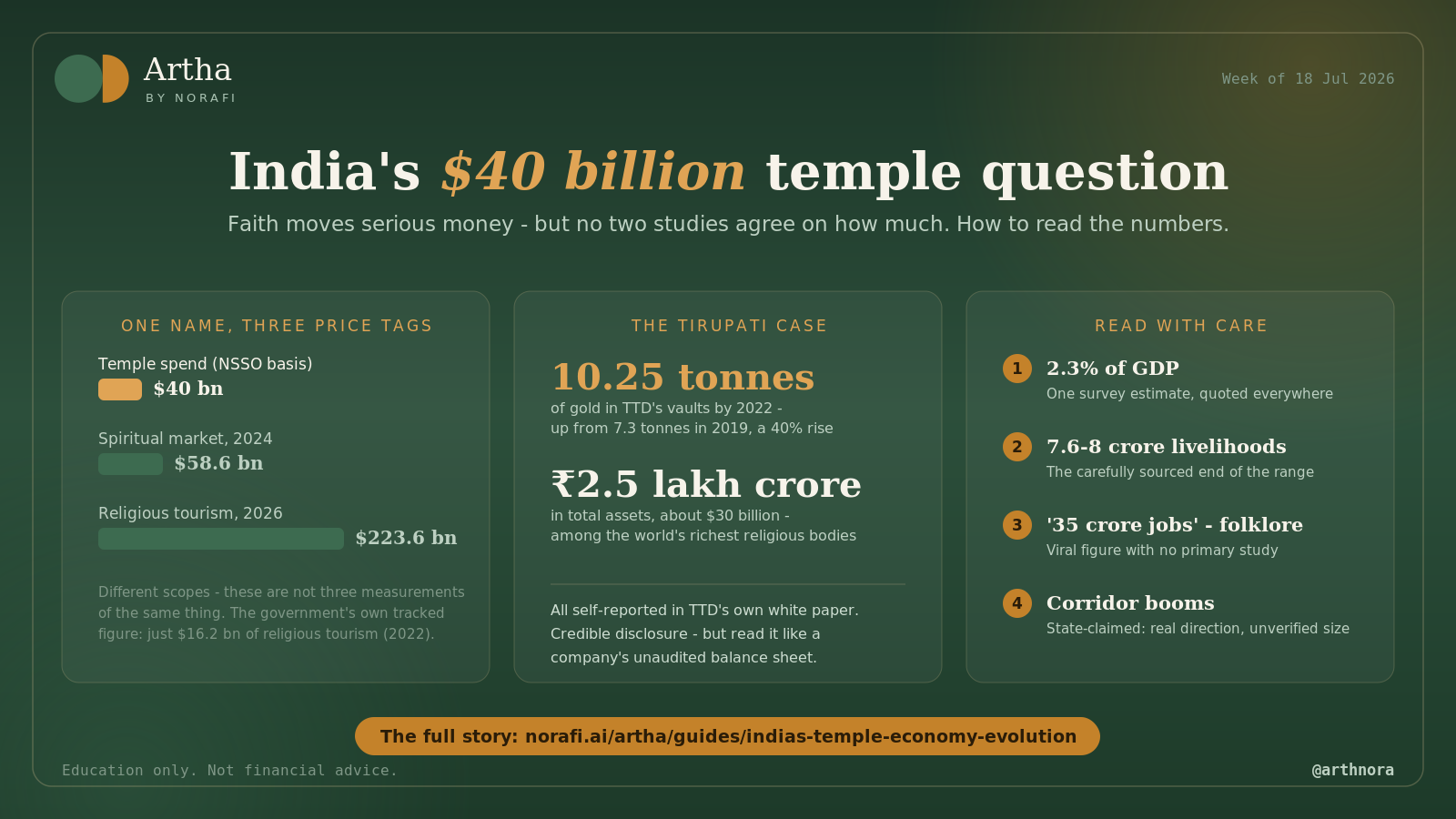

The most cited baseline traces back to National Sample Survey Office data on religious spending, which puts total Hindu pilgrimage expenditure at around Rs 4.74 lakh crore a year. A narrower reading of that same survey arrives at the figure most commonly repeated in press coverage: the temple economy proper, meaning direct spending in and around temples, valued at roughly Rs 3.02 lakh crore, or about $40 billion, close to 2.3% of GDP.

That is a single sourced NSSO derived estimate, repeated widely enough across academic papers and press pieces that it has become the default number, but it is worth treating as one data point rather than a settled fact, since the underlying survey methodology is rarely spelled out in the pieces that quote it.

Widen the lens to "religious and spiritual market," a category that folds in astrology apps, online puja services and spiritual retail alongside temples, and one market research estimate puts 2024 revenue at $58.56 billion, projected to nearly triple by 2034. Widen it again to the full "religious tourism market," and a 2026 industry report values that at over $223 billion, a figure built on tourism spend rather than temple revenue and covering a completely different set of activities, hotels, transport, retail, not the temples themselves. None of these three numbers should be read as three measurements of the same thing converging. They are three different objects being called by similar names.

The government's own tourism ministry numbers are narrower and more conservative still: religious tourism revenue was reported at $16.2 billion in 2022, up from $7.9 billion in 2021. That is the closest thing to an official, tracked figure in this entire space, and it is a fraction of the market research estimates above.

Chapter 2From temple land grants to government departments: how did we get here?

Temples were never purely religious institutions in India. Medieval and early modern temples, especially in the south, held land grants, ran agricultural estates, financed irrigation tanks and functioned as banks, lending out surplus grain and cash. The temple was often the largest single employer and landholder in its town.

Colonial administrators, uneasy with institutions that combined religious authority and large scale property, began legislating oversight rather than leaving that wealth to traditional trustees. The pattern continued after independence. Most major Hindu temples today are administered not by independent religious trusts but by state government endowment departments, under laws like Andhra Pradesh's Charitable and Hindu Religious Institutions and Endowments Act, which governs the Tirumala Tirupati Devasthanams even though TTD itself traces its formal administrative structure back to a 1933 act. This is a genuinely contested arrangement. Supporters of state oversight argue it professionalises administration of institutions holding public donations and prevents mismanagement by hereditary trustees. Critics, including groups like the Vishva Hindu Parishad, argue it is a lingering colonial structure that applies to Hindu institutions in a way it does not to mosques, churches or gurdwaras, which are largely self managed, and that it lets state governments treat temple surplus as a quasi public fund. Both positions have currency in current Indian political debate, and the article is not the place to adjudicate which is correct.

What changed more recently is not the ownership structure but the state's appetite for actively building around temples rather than merely administering them.

Chapter 3What actually generates the money?

Three broad income streams sit inside any large temple's books: cash and gold offerings through the hundi, income from land and property the temple has accumulated over centuries, and fees from services, special entry darshan, accommodation, prasad sales. Below the temple itself sits an informal economy of flower sellers, prasad makers, priests, guides, homestay owners and transport operators, the layer that NSSO adjacent research, including a 2024 study in the International Journal for Multidisciplinary Research, estimates supports something like 7.6 to 8 crore livelihoods nationally.

That figure needs a caveat the moment you see it next to other claims doing the rounds. At least one widely shared piece puts temple related employment at 35 crore people, more than four times the more carefully sourced estimate and larger than India's entire non farm workforce. No traceable primary study backs that higher number; it reads like the kind of dramatic, round, unsourced statistic the fact checking discipline in this newsroom exists to catch. Treat the 7.6 to 8 crore figure, itself only moderately well sourced, as the safer end of a genuinely uncertain range, and treat 35 crore as folklore until someone can point to the underlying survey.

The Tirumala Venkateswara temple is the cleanest single case study because it discloses more than most. TTD's own white paper reported gold deposits rising from 7.3 metric tonnes in 2019 to 10.25 tonnes in 2022, alongside total institutional assets valued at roughly Rs 2.5 lakh crore, about $30 billion, making it one of the wealthiest religious institutions on the planet. That valuation comes from the institution's own disclosure rather than an independent audit, so it belongs in the same sourcing tier as a company's self reported balance sheet: credible because TTD has strong disclosure norms by Indian trust standards, but not externally verified in the way a listed company's filings would be.

Are the new pilgrim corridors actually paying off?

The clearest recent shift in India's temple economy is state directed infrastructure spending built specifically around shrines, the Kashi Vishwanath corridor in Varanasi, the Mahakal Lok corridor in Ujjain, the Somnath and Kedarnath redevelopment projects, and the PRASHAD scheme funding smaller pilgrim towns, with 46 projects worth about $200 million sanctioned by early 2024.

The headline claim attached to the Kashi corridor is dramatic: an estimated Rs 1.25 lakh crore boost to Uttar Pradesh's economy since the corridor opened in December 2021, based on more than 25 crore devotee visits at an assumed spend of Rs 4,000 to 5,000 per visitor. That figure comes from the temple's own chief executive and a state university economist speaking to domestic press, not from an independent economic survey, and Uttar Pradesh's government has every political incentive to publicise a large multiplier from a project closely associated with the state leadership. It should be read the way you would read a hosting state's own multiplier estimate for a sporting event: plausible in direction, unverified in magnitude. What is independently trackable is the footfall itself, annual visitors to Varanasi were reported around 70 lakh before the corridor opened and have run many times higher since, though even that comparison varies depending on which government release you read, with cumulative visit counts cited anywhere from 13 crore to over 25 crore across different reports within the same year.

Chapter 5Does any of this actually move India's GDP?

Here the honest answer is that reasonable economists disagree, and the disagreement is worth stating plainly rather than picking a side. One view treats temple and pilgrimage spending as genuine economic activity with a real multiplier: money spent on a hotel room in Varanasi pays a housekeeper's wage, which gets spent again locally, and infrastructure like the Kashi corridor draws visitors, and their spending, who would not otherwise have come. The other view treats a meaningful share of this as substitution rather than creation: a rupee spent on a pilgrimage darshan package is often a rupee not spent on a different domestic holiday, and building a shrine corridor mostly reallocates existing tourism spend toward one town at the expense of others, rather than growing the national pie. Both arguments are standard tools from tourism economics, not unique to temples, and the NSSO adjacent data available today is not detailed enough to settle which effect dominates.

What is not in dispute is the direction of state policy. Whether or not the underlying multiplier holds up to scrutiny, the government is treating religious tourism as a deliberate growth lever, and the corridor building programme is the clearest evidence of that bet.

Faith has always paid its own bills in India. What has changed is that the state has decided it is worth actively marketing.